6 Important Financial Strategies for Your 20’s & 30’s

6 Important Financial Strategies For Your 20’s and 30’s

Personal Finance & Investing For Generations X and Y

Introduction

20 and 30-somethings have very different personal finance and investing priorities than their parents. Instead of worrying about Social Security benefits and catch-up IRA contributions, you might be worrying about digging yourself out of student loan debt, buying a house, or establishing yourself in a new career.

Retirement for Gen Y and Gen X investors is going to look very different than that of Baby Boomers. Today’s retirees can look forward to Social Security income, defined benefit pension plans, and the advantages of decades of stable work. The next generations of retirees may not have those assurances, making personal savings and investing, utterly critical. Continued health advances mean that average life spans are increasing. By the time you reach retirement age, your life expectancy may be such that you will spend over 30 years in retirement.

Early financial strategizing can help you get out of debt faster, save up for important life goals, and give you a head start on retirement. Here are six powerful moves that will help jumpstart your financial future.

1. Take Control of Your Health

You might think that the topic of your health doesn’t fit into a discussion of personal finance, but you’d be wrong. Medical bills resulting from illness and injury are one of the leading causes of bankruptcy in the United States.[1] If you’re not currently covered by health insurance, you should make it your first financial priority.

Studies show that young Americans (age 19-34) are the age group most likely to go without health insurance. As of 2011, 38% of young adults, approximately 18.5 million Americans, were uninsured.[2] If you are one of them, you may not have employer-sponsored insurance and don’t want to incur the costs of annual checkups and doctor’s visits.

Gambling on your health is a mistake. Avoiding medical visits can cause relatively minor medical or dental issues to worsen and become serious health and financial problems. Even if you’re generally healthy, a car accident or unexpected illness can bankrupt you.

Health insurance can help protect you from the financial consequences of a serious illness or injury and prevent you and your family from bankrupting yourselves. Fortunately, being young has many advantages, one of which may be lower insurance premiums. Basic health insurance doesn’t have to cost a lot of money. The health insurance landscape changed drastically with the Affordable Care Act (ACA.) If you are under the age of 26, you may be able to get coverage under your parents’ policy.

If you are not eligible for employer-sponsored or parental insurance, you can shop for health insurance plans on the ACA federal or state insurance exchanges by going to www.healthcare.gov. Depending on factors like your age, income, and health status, you may be able to qualify for lower monthly premiums that take the sting out of high healthcare costs.

2. Sharpen Your Negotiation Skills

If you’re like most Americans, you will make the majority of your wealth by working a job and collecting a paycheck. One of the savviest financial plays you can make early in your career is to learn how to negotiate a higher salary. Since subsequent raises and job offers will be based on your previous salary, you can drastically improve your lifetime wealth by setting a good standard early on.

Here are some negotiating tips:

- Don’t be afraid to ask for a raise or salary bump.

- Demonstrate why you’re worth more money.

- Do your homework so you understand what the market for your skills will bear.

- If you are initially refused a raise, ask for written goals and set a future date for another review.

- Think about alternatives to salary like performance bonuses and non-cash perks that can improve your lifestyle even if they don’t directly boost your earning potential.

3. Figure Out Your Financial Goals

Take a moment to think about the things you’d like out of life. Does your dream life include a house? Do you want to travel every year? Do you want your children to go to college? Whatever your personal goals are, chances are that they’ll take some preparation to get there.

When we think about saving and investing, most people’s minds immediately turn to retirement. While retirement is an important goal, there are also many intermediate life goals that require some financial strategizing to achieve.

Your goals might include:

- More education: College, graduate school, and advanced certificate programs can open doors and give your career prospects a serious boost. However, the costs of higher education are rising by about 3.0% per year.[3] Living expenses and foregone income will also raise the cost of education. Planning ahead can help ensure you have money set aside and don’t have to rely entirely on loans. If you’re already dealing with education debt, your goal might be to pay off your loans as quickly as possible.

- A house: Owning a house is still the dream for many young Americans. For most people, a house will be the largest purchase they ever make, so it’s worth planning ahead to save up for a down payment, learn about your credit score (and fix it if necessary), and study market trends in your area. An investment representative can help you run the numbers on renting vs. buying so you understand what the smartest move might be.

- A car: Saving up for a car avoids the necessity of qualifying for a car loan and making expensive payments each month.

- A sabbatical: An increasing number of Americans in their 20’s and 30’s are taking time off from their careers to travel, pursue passion projects, or make a difference in the world. If a career break is in your future, some advance goal-setting can help ensure that you have enough money set aside and don’t have to worry about finances while you’re out of the rat race.

4. Get Out of Debt

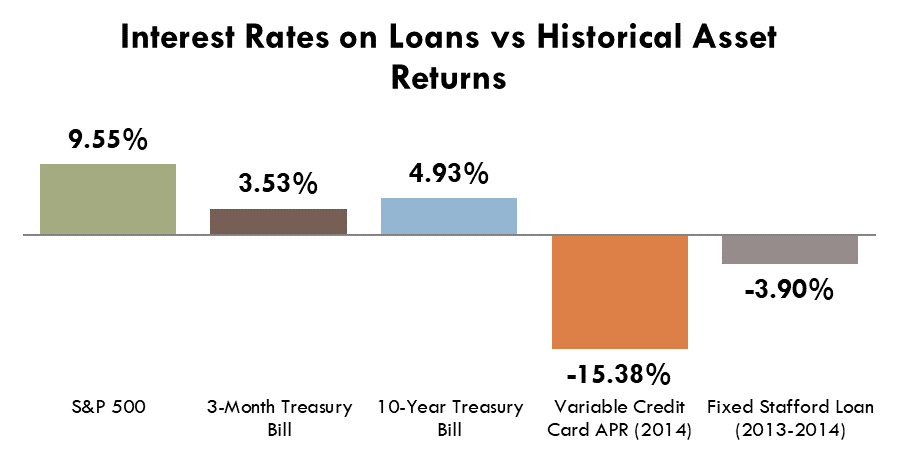

The average American under the age of 35 has between $23,000 and $30,000 of debt in the form of credit cards, student loans, auto loans, and other forms of personal debt.[4] The average U.S. household owes about $7,000 on its credit cards[5] and the average APR for variable-rate credit cards is over 15%.[6] This means that the average American family is making over $1,000 in interest payments each year.

If you are living with significant debt, paying it off is one of the smartest financial moves you can make. The reason for this is simple: You are likely paying more in terms of interest than you are likely to earn by investing.

The chart below illustrates historical returns for several different asset classes.

Source: NYU Stern, Federal Reserve of St Louis, Bankrate (March 17, 2014), ASA. S&P, 3-Month Treasury Bill, and 10-Year Treasury Bill historical geometric returns (1928-2013). Historical returns may exclude fees and expenses. The S&P 500 Index is an unmanaged index consisting of 500 common stocks of large-capitalization companies. Returns do not include dividend reinvestment. It is not possible to invest directly in an index. Past performance does not guarantee future results.

You can see that the historical performance of several common asset classes is dwarfed by the high APR on most credit cards. For most people, it makes sense to pay off that expensive debt instead of investing at lower rates of return. Every dollar that you contribute towards your debt reduces the amount of interest expense you have to pay each year and every year after that. Student loan interest rates are typically lower than most other forms of unsecured debt, making the decision about whether to pay down debt instead of investing more complex.

If you’re not sure whether to pay down your debt or start investing, a financial representative can explain the advantages and disadvantages of each option and help you make the right decision for your needs.

5. Protect Your Credit

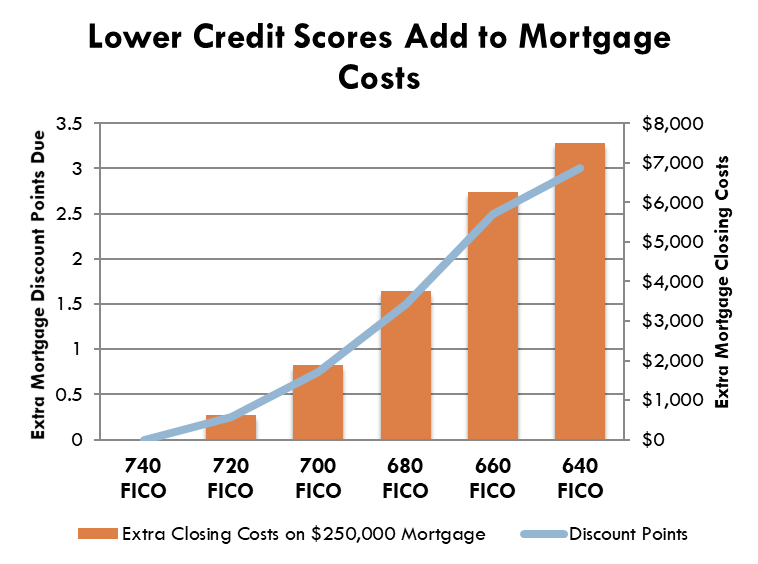

For better or worse, your credit score is one of the most important indicators of your financial health. Lenders, employers, and landlords – the list of people who have an interest in your credit score seems to keep growing every year. Damaged credit can be very costly over time. The chart below shows how discount points on mortgages are assessed based on credit scores.

Source: Trulia, Fannie Mae. Chart assumes conventional purchase mortgage and 20% down payment.

A $250,000 mortgage that’s assessed 1 loan discount point will have $2,500 in closing costs. Mortgage lenders give applicants with lower credit scores a higher risk rating, assigning them higher borrowing costs to make up for the greater potential risk of mortgage default. This calculation translates into higher closing costs; many people can’t afford to pay these extra costs at closing and choose to convert their discount points into an increased mortgage rate, raising the overall cost of the loan. Typically, every discount point can be converted into an extra 0.25% of mortgage interest.[7]

In short, the financial consequences of less-than-stellar credit can haunt you for decades. Unfortunately, there are no secret formulas or easy fixes for bad credit. Rehabilitation takes time and discipline, but it’s entirely possible to do.

Here are some simple steps that you can take now to rehabilitate and protect your credit:

- Check your credit report every year for free at annualcreditreport.com and dispute any errors.

- Pay all bills on time by setting up payment reminders or enrolling in autopay where possible.

- Avoid library late charges (anything that goes to collections gets reported to the credit bureaus).

- Pay down any balances on cards (high balances relative to your total available credit ding your credit score).

- Pay off your credit cards in full each month.

6. Save & Invest For the Future

Saving when you are still early in your career and may be living paycheck to paycheck is tough. There are a few strategies that can help you establish good saving behavior even when you don’t have a lot of extra income.

- Automate your savings: The simplest way to make saving unconscious and painless is to automatically direct a portion of each paycheck into your savings and investment accounts. You’ll quickly get used to having less money to spend each month and your savings will grow automatically.

- Focus on saving a percentage of your income: Even if you can only save 5% of your income, it’s an amount that will scale as your income grows.

- Build saving into your budget: If you include your monthly savings goal into your monthly budget, you’re much more likely to stick to your plan than if you simply save whatever money’s left over at the end of the month.

Along with saving, investing is one of the best ways to grow and protect your hard-earned wealth over the long term. When you’re in your twenties and thirties, retirement can seem like a long way off; but it’s important to start saving for retirement as soon as you can. Here’s a big reason why: the magic of compound interest.

Let’s say Joe is a 25-year-old investor who makes a single $5,500 contribution to a Roth IRA. If his portfolio earns an average rate of 8% per year, that single contribution could grow to $119,485 by the time Joe’s 65, even if he doesn’t add another dime to his IRA. However, if Joe waits until age 35 to start investing, that same $5,500 investment would only grow to $55,345. While this is a very simplistic example that discounts the effects of fees, inflation, and other factors, the basic principal is this: Time is one of the most important ingredients to long-term investment success.

Why invest? Putting your money to work for you through investing gives you a greater potential for return than saving alone. It’s important to understand that all investments involve some degree of risk. Understanding and managing risk is one of the most important pieces of a long-term financial strategy. Though it’s impossible to remove all risk from investing, professional investors use tools like diversification* and asset allocation strategies to help mitigate some risks.

The reward for taking on risk is the potential for greater investment return. If you have financial goals with long-term horizons (generally 5-10 years away), you may be able to accept additional risk by prudently investing in assets like stocks and bonds. Savings that are earmarked for short-term financial goals should generally be kept in cash or cash-equivalent securities. Keep in mind that it’s a good idea to speak to a qualified investment professional before making any investment decisions.

Today’s markets are volatile and many investors are worried that stocks may be too risky. In response to the financial crisis, many investors reacted to market turbulence by pulling out of the stock market and leaving their money on the sidelines. However, a portfolio that contains too little risk can reduce your potential for long-term growth and leave you vulnerable to inflation, which slowly eats away at returns each year. While stocks generally have a greater potential for loss than most bonds and fixed income investments, they also have a greater potential for gain over the long term.

As a long-term investor, it’s important to develop a clear understanding of your goals, risk appetite, and time horizon. One of the best ways a financial representative can help you is to assist you in developing a clear-eyed evaluation of risk and an investment strategy to help you mitigate it while still pursuing your long-term financial goals.

How Do I Take My Investing to the Next Level?

Financial representatives aren’t just for older, wealthier investors. They work with a variety of investors at all stages of life and can help you build a plan for the future. It’s very common for investors to start out investing on their own and then turn to a financial advisor when they want access to sophisticated tools, professional advice, and help developing targeted financial goals. A good investment representative can help you find the answers to important questions, like:

- Should I pay off my debt first, invest first, or both?

- How much should I be contributing to my company’s retirement plan?

- Do I need a Roth IRA?

- Which investments are right for me?

We hope that you’ve found this guide interesting and informative. While tackling all of these financial moves at once may seem overwhelming, focus on small steps and establishing good habits. Remember, there’s no better time than now to start taking control of your finances and make the most of your greatest resource: time.

We also want to offer ourselves as a resource to you, your friends, and your family. We are happy to answer questions about your current financial situation and future goals and we offer free consultations at any time. If you have any questions about the information presented in this report, please contact us. We would be delighted to speak with you.

Footnotes, disclosures, and sources:

Securities offered through SCF Securities,Inc. Member FINRA/SIPC 155 E. Shaw Ave. Suite 102, Fresno, CA 93710 • (800) 955-2517 •Fax (559) 456- 6109. SCF Securities, Inc. and Creative Financial Strategies LLC are independently owned and operated. www.scfsecurities.com Note: Securities offered through SCF Securities Inc., Investment Advisory Services offered through SCF Investment Advisors, Inc.

Opinions, estimates, forecasts and statements of financial market trends that are based on current market conditions constitute our judgment and are subject to change without notice.

This material is for information purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security.

Investing involves risk including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values.

Fixed income investments are subject to various risks including changes in interest rates, credit quality, inflation risk, market valuations, prepayments, corporate events, tax ramifications and other factors.

Opinions expressed are not intended as investment advice or to predict future performance.

Past performance does not guarantee future results.

Consult your financial professional before making any investment decision.

Opinions expressed are subject to change without notice and are not intended as investment advice or to predict future performance.

All information is believed to be from reliable sources; however, we make no representation as to its completeness or accuracy. Please consult your financial advisor for further information.