Is College Worth It?

Is College Worth It?

Understanding the Costs & Benefits of College

Introduction

The decision about whether or not to attend college is a serious one with lifelong implications. Changes in the U.S. economy, a decade of lost growth, and a revolution in technology are challenging attitudes about a traditional college education. While college used to be the default option for most high school graduates, a growing number of polls indicate that college is no longer the slam-dunk it used to be.

The high costs associated with getting a degree and the opportunity cost of spending four (or more) years in college, weighed against a weak job market, leave an increasing number of young Americans asking: is college still worth it?

The college debate is especially important for students who intend to stop at a four-year degree instead of continuing on to graduate or professional school. With recent growth in technical training, online education, and apprenticeship programs, some high school graduates may seek out more affordable alternatives to a traditional college path.

A 2013 Gallup poll found that 57 percent of U.S. workers don’t need an undergraduate degree and only half of white-collar workers believe a college degree is needed in their line of work. On the other hand, over two thirds of workers with professional, executive, or managerial jobs say a degree is needed in their jobs. [1] Another 2013 poll found that just 45 percent of respondents believe the cost of a college degree is justified, while 43 percent didn’t think college was worth the expense. [2]

This whitepaper will examine the costs and benefits of attending college today in order to help families and young Americans make an appropriate choice for their future.

The Costs of Attending College Today

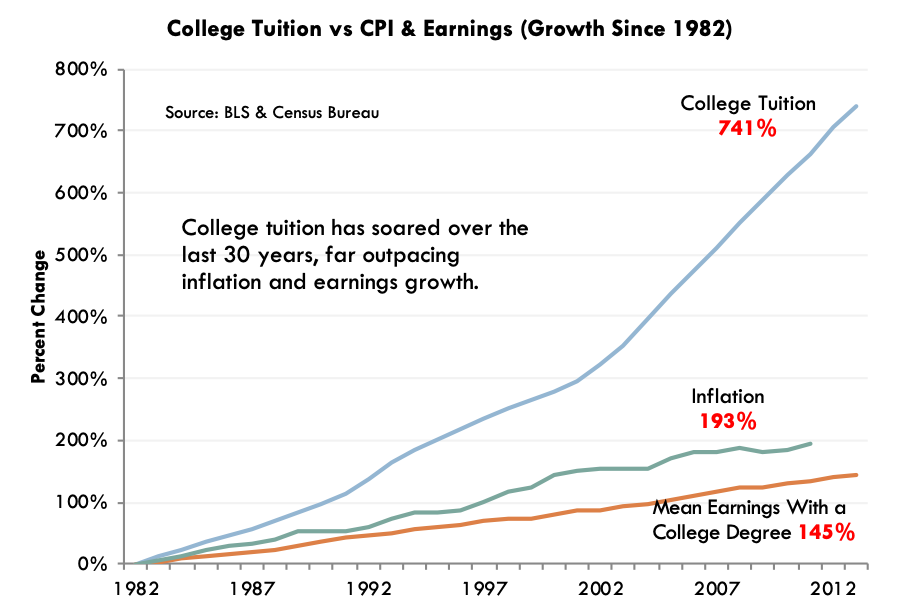

Student debt has skyrocketed and there is growing concern that a college degree is getting out of reach for many middle class Americans who find themselves in the financial aid gap: too wealthy to qualify for tuition assistance or federal financial aid, but not affluent enough to shoulder the full cost of a university. Unfortunately, growing college costs may make some families think that college is no longer a value proposition for them. Since 1982, college tuition costs alone have increased by over 700 percent, far outpacing increases in earnings for college graduates. [3]

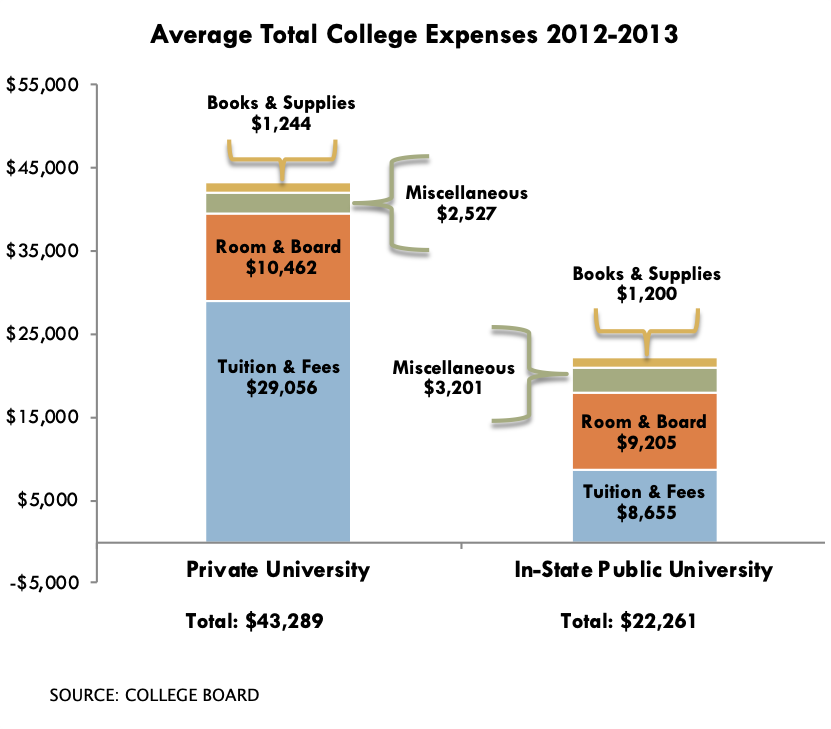

In a recent survey of college costs, the College Board reported that a “moderate” total annual budget for an in-state public school for the 2012-2013 averaged $22,261 while a moderate budget at a private college averaged $43,289. [4] Most universities will publish their tuition information; however, since tuition is only part of the total cost of attending college, it’s important to dig a little deeper to understand all the other expenses that go into a university’s total sticker price. Many universities will offer a similar annual breakdown to help you and your family understand the full cost of attendance:

- Tuition is what you pay a college for academic instruction. Fees run the gamut from student activity fees to parking and are typically mandatory. As you can see, tuition and fees vary widely between public and private colleges and financial aid is generally only applicable to this category of costs.

- The cost of room and board will depend on the level of housing and meal that that you choose. Most colleges will offer varying levels of meal support as well as on-campus and off-campus housing options. Of course, students that live at home can save a bundle on room and board.

- The books and supplies category includes everything from required books to classroom supplies and a computer.

- Miscellaneous expenses cover everything else: transportation, clothing, entertainment, insurance, etc. Every student lives a different lifestyle in college and it’s wise to consider a range of costs rather than a fixed amount.

The Benefits of College

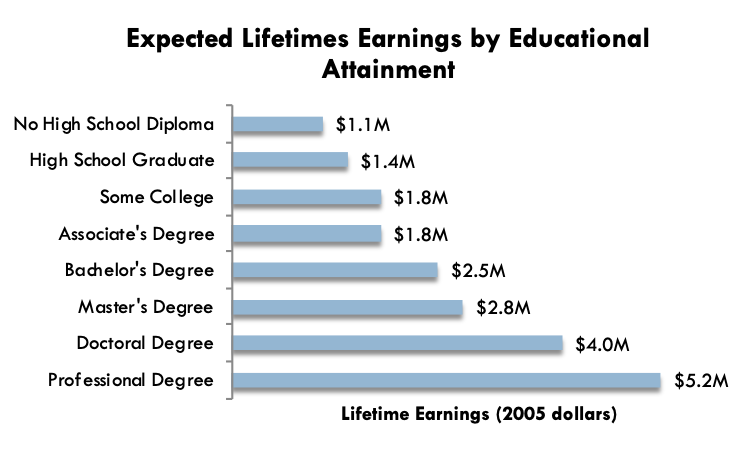

The economic case for college is simple: college graduates make more money. In fact, graduates with only an undergraduate degree make over $1 million more over the course of their lifetimes than Americans with just a high school diploma. Attaining a doctoral or professional degree can bump lifetime earnings into the $4 million and $5 million range. The majority of American high schoolers go straight to college, believing that a college degree will open the doors to high earning potential. These expectations are well founded: recent Gallup data shows a strong correlation between college degrees and high-income jobs. High school graduates and those with only a few years of college typically hold middle-to low-income jobs.[5]

Source: U.S. Census Bureau

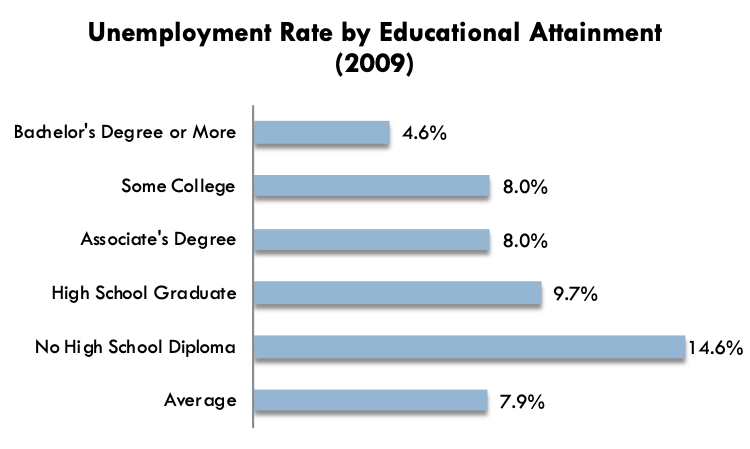

Americans with undergraduate degrees also have significantly lower rates of unemployment, which is beneficial during lingering recessions, when many workers are unemployed.

Source: U.S. Bureau of Labor Statistics

There are also more intangible benefits to getting a college degree, such as job satisfaction. Since we spend so much of our lives working, it’s important to feel good about the work that we do. According to a 2010 survey, people with higher levels of education are more satisfied in their jobs.[6] Another survey by the University of Chicago shows that the most satisfying jobs are: clergy, firefighters, physical therapists, teachers, engineers, psychologists, and education administrators – jobs that generally require advanced education to attain.[7]

Potential Drawbacks to College

While university can be a seminal experience for many young people, college isn’t for everyone. There’s no arguing with the fact that getting a degree can cost a significant amount of money and take a lot of time out of life. Some college graduates will be paying back their student loans for many years and may feel as though the value of their education wasn’t worth the time and expense.

Others believe that college may take time away from developing other skills, like entrepreneurship or technical skills not acquired in college. For example, there are many successful entrepreneurs who did not attend university or dropped out before getting their degree. Instead, they invested the time that peers spend preparing for a career building a successful business. Some students do not do well in college and drop out, compounding the issue of cost and time lost. College dropouts may acquire significant amounts of student loan debt while failing to benefit from the full value of a college degree.

While difficult to quantify, there can be consequences to sending an unprepared youngster to university. The college environment can be academically, emotionally, and mentally challenging and some young people are simply not ready to attend college when they graduate from high school. Pressuring someone into enrolling into college when they are not ready can lead to dropping out, poor grades, excessive major changing, and distress. A “gap year” between high school and college can help some young people find the focus needed to succeed in school. Others may benefit from attending a community college or taking classes part time before transferring to a four-year institution.

Ultimately, the decision about attending college is a deeply personal one that should be discussed well in advance of application time. If college lies in the future for you or someone you love, it’s important to plan for college as soon as possible.

Paying For College

Paying for college can put a serious strain on family finances, which is why it’s important to start planning early. It probably won’t surprise you to learn that the best way to trim a college bill is to start saving as soon as possible. While many families may plan to rely on financial aid to cover university costs, a recent study found that families who invest through a college savings plan will end up paying half as much as those who borrow.[8]

There are many ways to save for a child’s education and this list is by no means exhaustive; a financial representative can help you explore the options and come up with a strategy that fits your family’s needs.

Stafford Loans

Student loans are by far the most common way to pay for college. The chief benefit of loans is that students and their families don’t have to plan ahead for university expenses. Student loans typically rely on the student’s ability to find a well-paying job and pay back the loan. The obvious disadvantage is that relying too much on student loans will mean a heavy debt burden once the student graduates. Unfortunately, many students, excited about university and full of dreams for the future, do not think carefully about how student loans may affect their future employment prospects and lifestyle. It’s important to carefully read all loan paperwork and discuss loan terms with your child before making any decisions.

Congress recently reached an agreement to lower student loan rates for borrowers, making it less costly to fund an education. The bill only covers government-sponsored Stafford and PLUS loans, not loans available from private lenders. Each year, the rate for new loans will be set according to Treasury yields, meaning they will go up and down each year. However, once a loan is taken out, the rate is fixed for the entire term.[9]

Stafford loans are the most common form of government student loans and are awarded to college students who file the Free Application for Federal Student Aid (FAFSA.) They come in two forms: subsidized and unsubsidized. While both types are fixed-rate loans, subsidized loans have the benefit of accruing no interest while the student is enrolled, while unsubsidized loans begin accruing interest immediately.

PLUS loans are another type of federal loan available to parents of dependent undergraduates that can be used to cover student expenses not covered by other forms of financial aid. The maximum that can be borrowed is the student’s cost of attendance (as determined by the school) minus any other financial aid received.

529 Plans

Another option for saving towards a child’s education is a 529 plan. These plans are legally known as “qualified tuition plans” and allow money to grow and be withdrawn federally tax-free when used for qualified postsecondary education-related expenses. Their popularity is increasing; according to data from the Financial Research Corporation (FRC), 5.5 million U.S. households had 529 plans in 2012 as compared to 3.5 million five years ago.[10]

There are two main types of 529 plans, pre-paid tuition plans and college savings plans. Both types of plans are typically sponsored by states, state agencies, or educational institutions. 529 plans can be a great way to help save money for college because they carry a number of tax benefits, depending on the state in which you live. Another of their advantages is that the account owner (often a parent or other relative) retains control over the account, even when the beneficiary (the student) is no longer a minor. If your child qualifies for financial aid and the 529 funds are no longer needed, they can be easily transferred to another beneficiary and used for his or her education.[11]

Prepaid tuition plans are 529 plans that are guaranteed to increase in value at the same rate as tuition at participating colleges in your state. They allow families to purchase units or credits at local private and public universities for future tuition (and sometimes room and board.) The idea is that you can pay for future tuition at today’s prices. They are frequently backed by the full faith and credit of the state.* The obvious downside is that, to gain the full benefit, a student must be willing to enroll in a school covered by the 529 plan. While it is often possible to transfer tuition credits out of state, the plan will not offer the same level of tuition support, leaving the family to make up the difference. [12]

529 college savings plans are tax-exempt savings vehicles that allow families to invest for future college expenses. Unlike prepaid tuition plans, there are no guarantees and investments are subject to market conditions. However, with these added risks comes the opportunity for potentially greater returns.

529 plans are subject to contribution limits, depending on the state that sponsors the plan. Many states limit total contributions, meaning that once that limit has been reached, (including earnings) no more contributions will be accepted. 529 plans can also be subject to gift tax limits; any amount that you contribute over the annual gift exclusion amount may be subject to federal gift taxes.[13] Donors may be able to accelerate transfers to a 529 plan without incurring federal transfer taxes, but the process is complex. A tax professional can help you understand whether this is a good choice for you. Withdrawals from 529 plans that are not used towards qualified education expenses may be subject to penalties and taxes.

It’s important to consider the impact that savings will have on financial aid calculations. 529 college savings plans may not have a big effect on your ability to qualify for support. In the financial aid formula, a 529 plan is treated as a parental asset, meaning that only 5.64 percent of the value is applied towards the family’s expected contribution. In contrast, assets held in the child’s name (such as in UTMA/UGMA accounts) get assessed at 20 percent. An important caveat is the difference in treatment when the 529 plan is owned by someone other than a parent or student – such as a grandparent. In that case, any distribution from that 529 plan is reported as income to the beneficiary, potentially resulting in a reduction in eligibility for need-based financial aid the following year.[14]

*Participation in a 529 Plan does not guarantee that the contributions and investment returns will be sufficient to cover future higher education expenses. Investments involve risk and you may incur a profit or a loss. There is no guarantee that Dollar Cost Averaging will result in a profit or protect against a loss in a declining market. Investors should carefully consider the investment objectives, risks, charges, and expenses of the municipal fund before investing. This, as well as other important information, is contained in the official statement. Please read it carefully before insetting or sending money. An investor’s home state may offer favorable tax treatment only for investing in a plan offered by such state. Withdrawals for non-qualified expenses may be subject to additional penalties and taxes. Consult your tax advisor regarding state and federal tax consequences of the investment.

UTMA/UGMA Accounts

The Uniform Gifts to Minors Act (UGMA) and the Uniform Transfers to Minors Act (UTMA) are two types of custodial accounts that adults can set up on behalf of minors for college. Parents, relatives, and friends can contribute to the account and all of the assets (e.g. mutual funds, stocks, bonds, CDs, etc.) are turned over to the beneficiary’s control at age 18 or 21 (depending on the state in which it was opened.) The main benefit of this type of account is that the assets can be used for any purpose, not just college tuition. There are also no contribution limits, though contributions above the annual gift tax exclusion may incur federal gift taxes.

Here are a few important things to consider with UTMA/UGMA accounts:

- Any transfer into this type of account is irrevocable and it is not possible to transfer money back to the parent. Once the money has been given to the child, the child owns it.

- UTMA/UGMA accounts are not tax-deferred. You may need to file tax returns on the minor’s behalf. Consult a tax professional for more information.

- No restrictions can be placed on the use of assets once the minor becomes an adult. At that time, the beneficiary can use the money for any purpose.

- Since UTMA/UGMA accounts are in the name of a single beneficiary, they are not transferable to another beneficiary.[15]

Coverdell Education Savings Accounts

Coverdell ESAs are another option that may be attractive college savings vehicles, particularly for families who also wish to save for their child’s K-12 education. Coverdells function in a similar way to Roth IRAs, in that funds are contributed after tax and grow tax-free; distributions are also tax free, as long as they are used for qualified educational expenses. Under IRS regulations, a beneficiary is someone who is under age 18 or has special needs. Here are some important things to consider:

- Total contributions per child cannot exceed $2,000 per tax year, even if they are made by different family members.

- Coverdells cannot be funded once the beneficiary reaches age 18. The account must be fully withdrawn by the time the beneficiary is 30, or remaining funds may be subject to taxes and penalties.

- Like 529 plans, parents (or account custodians) retain control over the account assets, but they must be used for the benefit of the beneficiary and cannot be transferred back to the adult or another beneficiary. [16]

However your family chooses to cover the expenses of college, it’s important to speak with a financial professional who understands your unique circumstances, goals, values, and time horizon and can help you determine financial and investment decisions for your family. There are many important factors that will impact your choice of college savings vehicle, not least of which is its financial aid treatment. Parental income factors heavily in financial aid calculations, which can be a double blow to families with higher income but no college savings. As much as 47 percent of income can be counted toward a family’s expected contribution, meaning that middle-class families frequently get caught in the financial aid gap; they make too much money to qualify for aid but cannot afford to pay the full price for university expenses.[17]

In financial aid calculations, custodial accounts like UTMA/UGMA accounts (and sometimes Coverdells) are considered assets of the student and may have a higher impact on financial aid eligibility than non-custodial accounts like 529 plans.[18] There are a number of strategies that may help reduce the impact of college savings plans on financial aid calculations and a financial representative can help you develop a plan that is right for your needs.

How a Financial representative Can Help

For many families, paying for college can be a daunting task, but professional financial advice can help you make decisions for your child’s future. Financial representatives don’t just help clients strategize for retirement; we help our clients develop strategies to address all of life’s major financial milestones, including paying for college.

We hope that this report has been useful to you and your family; we recommend sharing it with your child or any family member that is weighing the benefits of enrolling in college. While the decision to attend college is a major one, we believe that being well informed is key to making the choice that’s right for you and your family.

Footnotes, disclosures and sources:

Securities offered through SCF Securities,Inc. Member FINRA/SIPC 155 E. Shaw Ave. Suite 102, Fresno, CA 93710 • (800) 955-2517 •Fax (559) 456- 6109. SCF Securities, Inc. and Creative Financial Strategies LLC are independently owned and operated. www.scfsecurities.com Note: Securities offered through SCF Securities Inc., Investment Advisory Services offered through SCF Investment Advisors, Inc.

Opinions, estimates, forecasts and statements of financial market trends that are based on current market conditions constitute our judgment and are subject to change without notice.

This material is for information purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security.

Investing involves risk including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values.

Fixed income investments are subject to various risks including changes in interest rates, credit quality, inflation risk, market valuations, prepayments, corporate events, tax ramifications and other factors.

Opinions expressed are not intended as investment advice or to predict future performance.

Past performance does not guarantee future results.

Consult your financial professional before making any investment decision.

Opinions expressed are subject to change without notice and are not intended as investment advice or to predict future performance.

All information is believed to be from reliable sources; however, we make no representation as to its completeness or accuracy. Please consult your financial advisor for further information.