Long-Term Care Insurance Premium Deductibility

According to IRS Revenue Procedure 2020-45, a couple age 70 or older who both have the right kind of long-term care insurance policy can deduct as much as $11,280 in 2021 an increase of $420 from the $10,860 limit for 2020. Essentially, more of the premiums you pay will be deductible. If you own a policy or are considering buying one, here are a few things to know.

The premiums are tax-deductible for the taxpayer as long as they, along with other unreimbursed medical expenses, exceed 7.5% of the insured’s adjusted gross income. Someone self-employed can take the amount of the premium as a deduction as long as they made a net profit. There’s a limit on the deduction allowed based on the taxpayer’s age at the end of the year, and any premium amount above these limits isn’t considered a medical expense.

The nitty-gritty of making deductions:

- The policy must be considered “tax-qualified”

- You’ll need to itemize deductions on a Schedule A to claim a deduction for medical expenses paid out of pocket

- You can only deduct the amount of medical expenses that exceed 7.5% of your adjusted gross income

- The amount that can be claimed as a medical expense depends on the policy holder’s age

- If you’re self-employed, it’s possible to write off the premiums as a business expense rather than an itemized medical expense

- If you own an asset-based or hybrid LTC policy, the extension rider or “true LTC” portion of the premium is the part eligible for deduction. Check with your financial professional to determine the type of policy you own

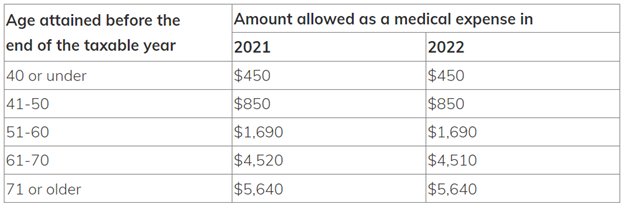

2022 Long-Term Care Insurance Deductible Limits Per Individual1

There is a limit on how much of the premium can be deducted depending on the age of the taxpayer at the end of the year. Any premiums above these amounts are not considered to be a medical expense. For example, if you’re 55 and pay $2,000 a year in long-term care premiums, only $1,690 of what you paid would be deductible in 2022. If you were 65, though, the full $2,000 would be deductible because of the higher limit at that age.

The tax benefits of a long-term care insurance policy is something to take into account if you’re looking to purchase. As your trusted financial professional, we are here to help get you the information you need to make an informed decision.

Adapted from ElderLawAnswers1

Adapted from Forbes2